By Mariana Villalba, CFA

The ongoing conflict in Iran and its expansion across the region to target GCC countries unfolded following a period of debt-issuance growth in the region, especially from the financials sector.

As the conflict continues, we believe a deeper dive into GCC financials is warranted. Below, we take a closer look at GCC banks, which represent about one-tenth of the J.P. Morgan CEMBI Broad Diversified’s[1] market capitalization.

GCC Diversification From Oil to Credit

Over the past few years, Gulf GCC countries have been actively pursuing economic diversification away from the hydrocarbon sector and pursuing social transformation by attracting foreign human and financial capital into the region.

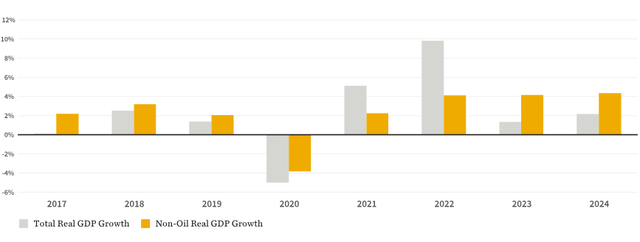

This is evidenced by the performance of non-hydrocarbon economic growth, which has outperformed real gross domestic product (GDP) growth in recent years, as the chart below shows.

Real GDP Growth of the Non-Oil Economy in GCC States (Year-Over-Year Change)

Source: IMF Database: Middle East and Central Asia Regional Economic Outlook.

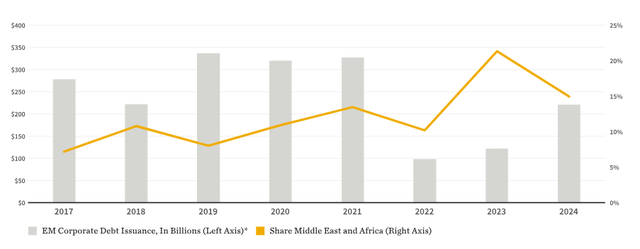

Increased public debt issuance has accompanied economic diversification. The first chart below shows the Middle East’s share of emerging markets (EM) corporate primary debt issuance since 2017.

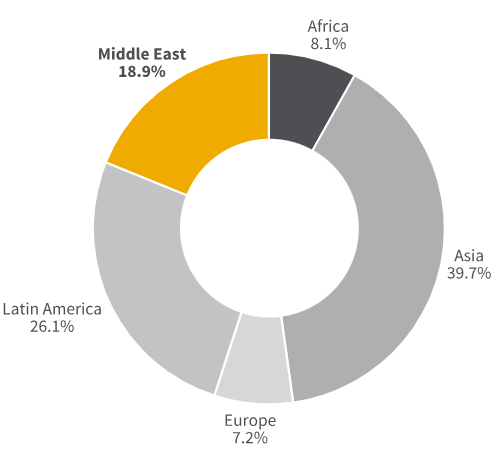

The second chart shows that as of December 2025, the Middle East made up nearly one-fifth of the J.P. Morgan CEMBI Broad Diversified’s market capitalization, of which GCC countries represented more than 80%. The financials sector accounted for about half of the region’s exposure.

EM Corporate Debt Issuance

Source: J.P. Morgan, as of December 2025. Universe is the J.P. Morgan CEMBI Broad Diversified. *Excludes 100% government-owned entities.

Regional Breakdown of the Index (Percentage of Market Capitalization)

Source: J.P. Morgan, as of December 31, 2025. Universe is the J.P. Morgan CEMBI Broad Diversified.

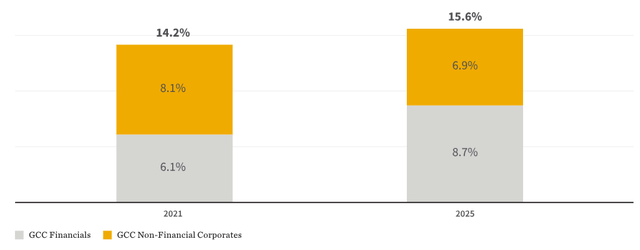

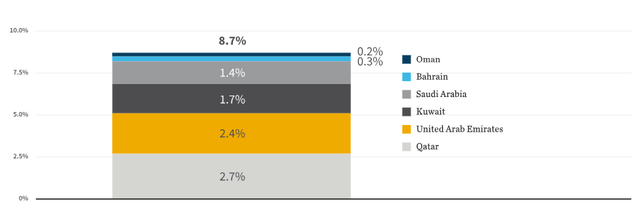

Increased debt issuance from the financials sector has driven the region’s issuance growth. As a result, the share of GCC financials in the index has risen by more than 2.5 percentage points to nearly 9% since 2021, as shown in the chart below. This growth was mainly driven by issuers in Saudi Arabia, UAE, and Kuwait.

GCC Market Cap (Financials vs. Other GCC Non-Financial Corporates)

Source: J.P. Morgan, as of December 31, 2025. Universe is the J.P. Morgan CEMBI Broad Diversified.

GCC Financials Breakdown by Country (Percentage of the Index)

Source: J.P. Morgan, as of December 31, 2025. Universe is the J.P. Morgan CEMBI Broad Diversified.

How the Conflict May Affect GCC Banks

After years of stability that fostered a supportive operating environment, the ongoing conflict in Iran and its expansion across the region into GCC countries may pose challenges to the pillars of the region’s growth strategy and to banks in the region.

In our view, there are three main channels through which the conflict may impact banks in the region. The degree of impact may vary depending on each bank’s business model, level of diversification, and overall strategy.

Loan Growth. We believe the most immediate and direct impact of the conflict on the banking sector is its negative impact on economic activity due to physical disruption, infrastructure destruction, and lower consumer and corporate confidence.

This may impact banks’ lending growth and potentially revenue generation. From a credit investor’s perspective, however, a slowdown in lending growth might be positive from a capital perspective, although there are other factors that could offset that positive effect.

Funding. This is another potential channel of impact, both in terms of liquidity availability and cost of funding. As energy prices have risen, global rates have risen and financial conditions have tightened.

Both institutional investors and depositors may become more risk-averse and require a higher premium to provide funding to banks in the region. Additionally, the economic disruption caused by the conflict might reduce companies’ cash flows and hence the volume of deposits in the financial system.

Asset Quality. A slowdown in economic activity and damage to physical infrastructure may weaken the creditworthiness of borrowers and impact their ability to repay their debts, reduce the value of collateral, and even lead to defaults. This could entail additional provisioning requirements from banks and increase the balance of non-performing loans (NPLs).

While risks abound and the level of uncertainty is high, we believe GCC banks could benefit from strengths that allow them to navigate this turbulent period relatively well from a credit perspective. These include strong balance sheets, favorable ownership structures, and a supportive regulatory environment.

Strong Balance Sheets

GCC banks came to the conflict in a position of fundamental strength. The median NPL coverage of banks in the region was 150%, according to our analysis, which indicates that there is room to absorb some asset-quality deterioration.

At the same time, banks maintained a median capital buffer of more than 400 basis points above minimum requirements across the GCC,[2] and more than 300 basis points when excluding Saudi Arabia. That should alleviate concerns about solvency, even in the absence of extraordinary support.

One caveat pertains to dispersion. Individual banks may have weaker credit fundamentals than the aggregate data suggests and hence be more vulnerable to shocks. However, these banks represent a smaller part of our investment universe.

Supportive Ownership Structures

Most banks in the region have government ownership, often through controlling stakes. In turn, the creditworthiness of most GCC sovereigns is very strong, as evidenced by high credit ratings, relatively low debt levels, and high foreign exchange reserves.

Combined, these factors translate into a strong ability and willingness to support local banks. This is often explicitly reflected in banks’ credit ratings, with many benefiting from rating uplifts directly as a result of their ownership structure.

Supportive Regulatory Environment

In addition to the expectations of support embedded in the credit rating agencies’ assessments we described above, bank regulators and central banks in the region have a track record of providing support to the banking sector in events of stress. This happened during the COVID-19 period.

Following the start of the Iran conflict, regulators in the UAE, Qatar, and Kuwait came out with measures of support and/or relief for their respective banking sectors, with the UAE providing the most comprehensive plan.

These measures include, among others, 1) temporary relaxation of liquidity and capital requirements; 2) provision for additional liquidity facilities; 3) temporary flexibility for bad-loan recognition; 4) temporary easing of reserve requirements; and 5) payment relief for borrowers.

While we are not downplaying the economic and human cost of the conflict, which are significant and should not be neglected, we remain comfortable with the fundamentals of GCC banks, which should support relative resilience through this turbulent period.

[1] The J.P. Morgan CEMBI Broad Diversified is a widely used benchmark that tracks the performance of U.S. dollar-denominated corporate bonds issued by companies in EMs.

[2] Does not consider pillar 2 requirements applicable in Saudi Arabia, which are not publicly disclosed.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here